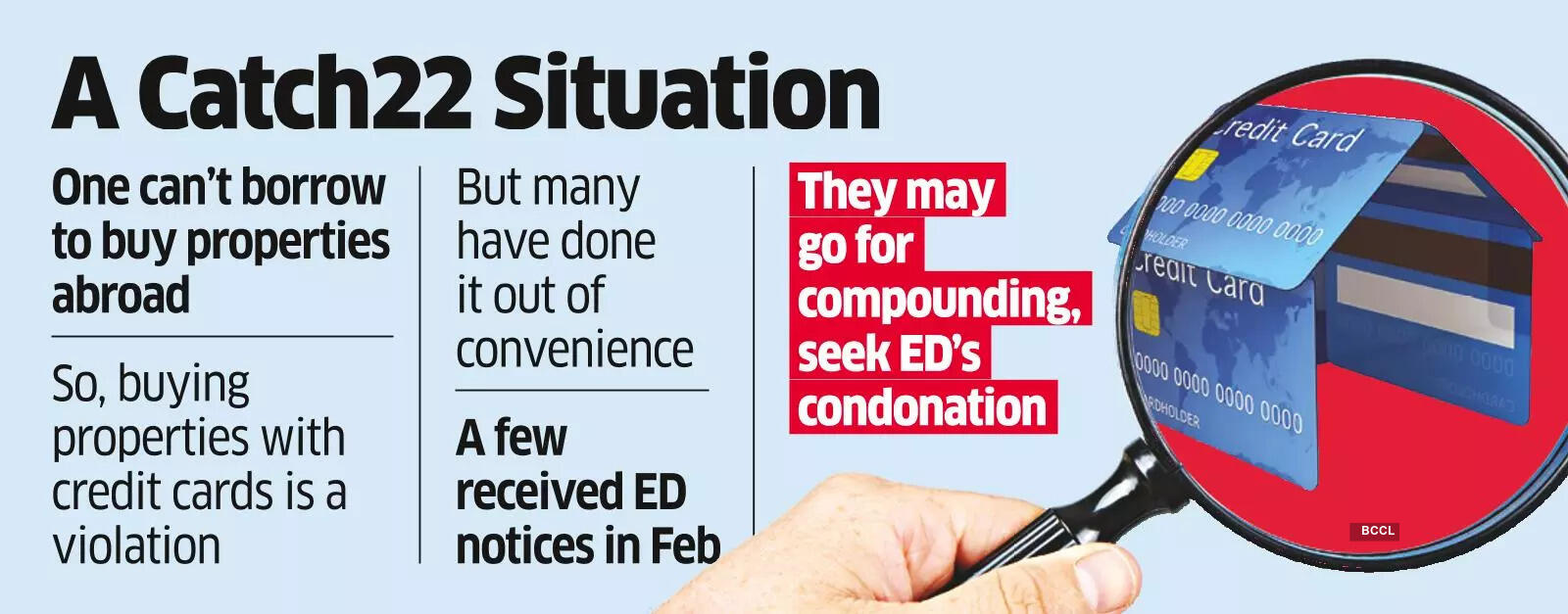

MUMBAI: As rain dampens Dubai, the property market faces stress, prompting Indian buyers who used credit cards for their purchases in Dubai to receive notices from the Enforcement Directorate (ED).

These buyers often used international credit cards (ICCs) during their visits to the Emirates for initial deposits or clicked on developer-sent payment links, likely unaware that they were violating Indian laws.

Sources indicate that at least three individuals received notices from the ED in February, inquiring about the source of their funds for these transactions. Credit card transactions are treated as short-term loans, and foreign exchange regulations restrict individuals from borrowing money to purchase overseas properties. The Reserve Bank of India’s (RBI) liberalized remittance scheme (LRS), which allows residents to invest in stocks and apartments abroad, mandates that tax-paid funds must be transferred through official banking routes.

Those who received notices and are looking to correct their transactions face a dilemma. They must navigate the challenges of rectifying the payment, paying penalties, and possibly selling the property in a declining market, as trust in Dubai’s status as a safe haven wanes.

“The recent ED notices target individuals who may have unknowingly used credit cards to purchase UAE properties. They should consult the RBI to regularize their payment methods. Considering the funds are legitimate, the RBI might adopt a lenient stance,” stated Rajesh Shah, partner at the CA firm Jayantilal Thakkar & Co., specializing in forex and anti-money laundering regulations.

Before seeking a compounding process—admitting to violations and paying a penalty—the administrative procedure must be fulfilled. This may involve reversing the initial payment in certain cases.

“The regularization process might include remitting new funds via banks and asking the builder to refund the initial credit card payment. In some cases, the RBI may require buyers to sell the property and repatriate the funds,” Shah explained.

This, however, requires arranging funds without borrowing and remitting dollars at a time when the rupee is at a new low. If this proves unfeasible, buyers might be forced to sell their properties to untangle the transactions. However, bankers believe the regulator may not insist on reversals since the funds did not originate from hawala operations.

“Utilizing international credit cards (ICCs) for such acquisitions strays outside the allowed framework, as overseas property acquisition is considered a ‘capital account’ transaction. Individuals who have made these payments need to explore regularization avenues, including the RBI’s compounding process,” said Moin Ladha, partner at Khaitan & Co.

ICCs are intended for current account transactions like purchasing books, downloading movies, and booking hotels, much like local cards.

According to Pankaj Bhuta, founder of the CA firm P. R. Bhuta & Co, even if the ED has initiated actions against an individual, they can still opt for compounding before the RBI until the conclusion of the adjudication process. “Compounding usually requires no objection from the ED, which has granted permission in recent instances when it aligns with the intent of the Foreign Exchange Management Act (FEMA). In such scenarios, the RBI can limit the compounding fee to ₹2 lakhs,” said Bhuta.

Under the LRS, individuals can remit up to $250,000 yearly to acquire assets abroad or shop online from India. Some who resorted to ICCs for property acquisitions may have done so to safeguard their annual LRS limits.